Financial Abuse Risk for Seniors Isolated by Pandemic

Each year, senior citizens lose billions of dollars to financial fraud, with the loss to individual victims averaging tens of thousands of dollars.

Each year, senior citizens lose billions of dollars to financial fraud, with the loss to individual victims averaging tens of thousands of dollars.

The death care industry — yep, it’s got its own industry moniker — is an estimated $20 billion business. Service Corporation International, a publicly traded company that operates 1,475 funeral homes and 483 cemeteries in 44 states, pulled in more than $3.2 billion in revenue in the past 12 months.

Anderson Cooper’s newborn son Wyatt started life with every material advantage and a lot of big questions. Call it the Vanderbilt Curse.

It can be hard to move through your daily life after someone you love dies. It may be even harder to embark on the complex tasks required to put their financial affairs in order. However, you can’t afford to put that off.

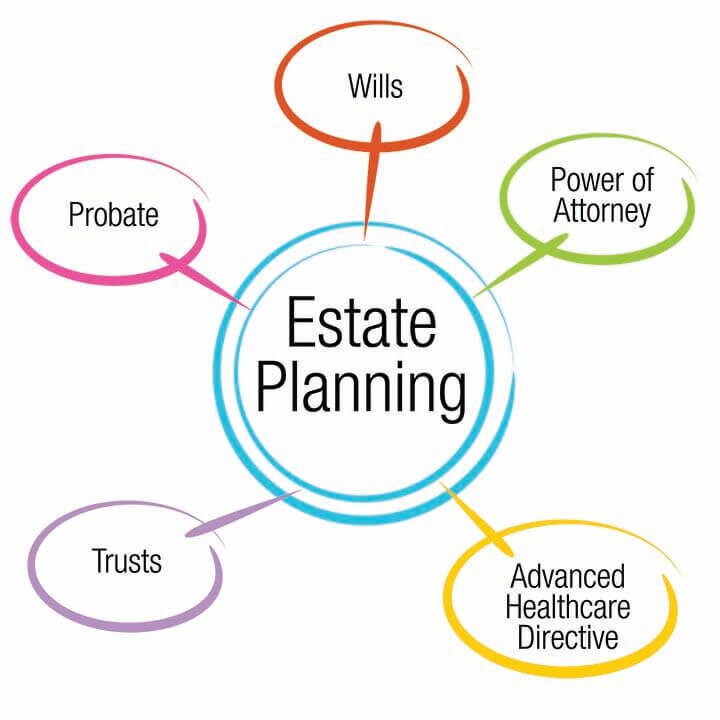

Too many people mistakenly believe that to have a need for estate planning, you must be old and wealthy. Nothing could be farther from the truth. Once you are a mature adult, independent, and income-producing, it is time to assume the responsibilities of preparing for your future. High on the list is preparing an estate plan with a clear understanding that your plan will be revised to adapt to changing circumstances.

Without an estate plan in place, clients will be reliant on state laws and probate courts to appoint individuals who will be responsible for financial affairs and health-care decisions, in the case of illness and ultimately the transfer of assets upon death.

Estate planning is the process of arranging, while you are alive, what will happen to your estate, your children and your wealth after you die.

COVID-19 is quickly becoming the leading cause of death in the United States. As of today, Indiana has over 37,000 cases of COVID-19 and over 2,100 deaths. That is why articulating your wishes regarding end-of-life health care, is more important than ever.

If you want a legal plan that avoids probate court, there are two options: first, an enhanced life estate deed, and second a living trust. Each has its pros and cons.

Beneficiaries of a trust typically pay taxes on the distributions they receive from the trust’s income, rather than the trust itself paying the tax. However, these beneficiaries are not subject to taxes on distributions from the trust’s principal.